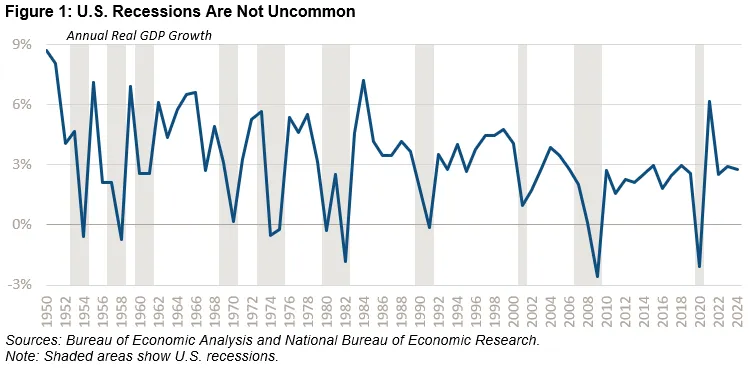

The U.S. has never experienced an economic shock as indebted as we are today. Recessions and other economic shocks are inevitable. Although the timing and particulars of the next downturn or emergency are hard to anticipate, one can predict with certainty that another will occur eventually. In almost any case, the shock and response will worsen the nation’s already unsustainable fiscal situation.

Unfortunately, the U.S. has far less capacity to address the next shock than it has previously. The national debt increased by a combined 65% of Gross Domestic Product (GDP) over the past two recessions and recoveries, with the federal government entering them with debt at 35% and 80% of GDP, respectively. Today, debt totals 100% of GDP – only a few percentage points from the previous record set after World War II. This situation leaves the U.S. immensely vulnerable.

In light of this precarious fiscal situation, policymakers should act carefully and judiciously when the next shock occurs. Too often, lawmakers wait for the emergency to happen before thinking through how they might react. Then, once the economy recovers, they move on. These crisis-driven responses can be costly and haphazard and, in some cases, may solve one problem while creating another.

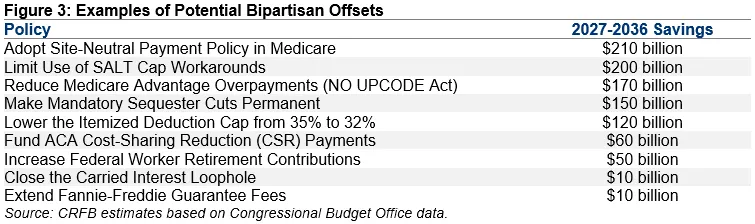

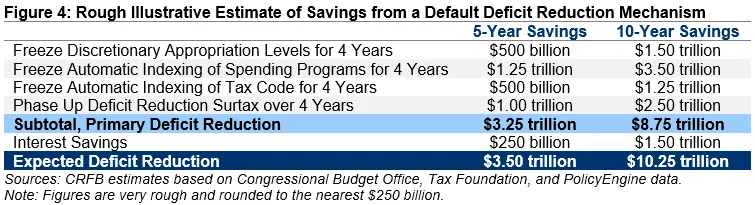

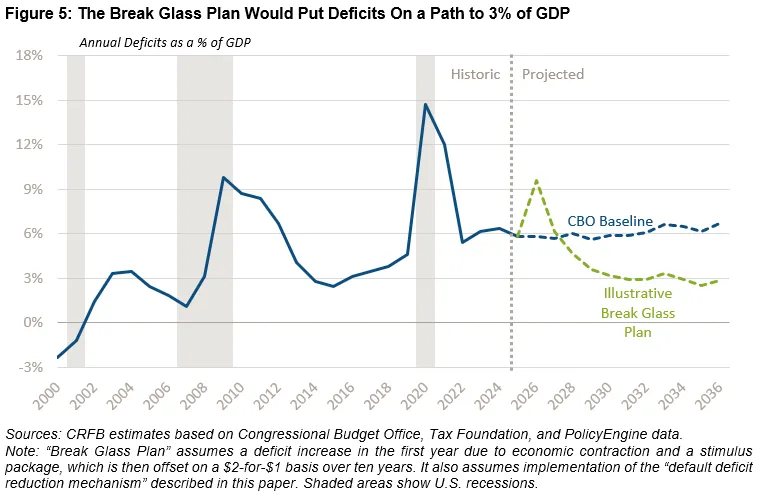

To help guide thinking in the moment, lawmakers should prepare a Break Glass Plan that is ready to deploy when the time comes. Such a plan could include:

Whether rising debt is the source or symptom of the next shock, a thoughtful response should include solutions that reduce deficits and stabilize the debt to reassure markets and buttress economic resilience for households.